Geoeconomic fragmentation, the phenomenon of division of the global economy into regional competing blocs, has been growing since the 2008-2009 Global Financial Crisis. It has intensified over the past eight years, driven by governments and businesses aiming to protect against supply chain disruptions and rising trade barriers.

In 2025, geopolitical shifts, including conflicts in Europe and the Middle East, ongoing US-China tensions, and evolving supply chain trends, are expected to accelerate this fragmentation, facilitated by protectionist policies, which are policies that look to restrict international trade to protect domestic industries from foreign competition. This includes trade barriers such as tariffs, quotas, and subsidies that make imported goods more expensive or less competitive. Notable examples include the EU’s Digital Tax targeting large technology companies, China’s “Dual Circulation” strategy promoting domestic consumption and technological self-reliance, and India’s elevated tariffs on electronics and solar panels to foster local manufacturing. US President-elect Donald Trump has also recently demonstrated his strategy of using protectionist policies to likely have better negotiating power as even before his inauguration he threated increased tariffs including 25 percent on goods from Mexico and Canada, 60 percent on Chinese imports, and 100 percent on products originating from BRICS nations.

In response to these supply chain vulnerabilities, resource nationalism will likely rise. Resource nationalism is the aspect of countries increasingly asserting control over their natural resources through policies that limit foreign ownership or influence. This trend includes measures such as nationalization, resource taxes, export restrictions, higher royalties, and stricter regulations on foreign companies operating in resource sectors. EU has exemplified this by initiatives like the European Raw Materials Alliance and the EU Critical Raw Minerals Act, which aim to reduce dependence on external mineral sources by fostering intra-European resource development and trade. In the USA, policies such as the CHIPS and Science Act and the Mineral Security Partnership with allies like Australia and Japan reflect efforts to secure critical minerals and decrease reliance on China. Looking ahead, countries will further move towards prioritizing domestic and allied resource development to mitigate the impact of external risks posed to local economies.

With this, global trade flows are anticipated to adapt rather than collapse under rising protectionist measures. Connector countries like Mexico and Vietnam, serving as strategic hubs between regions and economies, are poised to mediate trade between countries like the US and China, which have curtailed trade despite past interdependence in critical sectors such as technology, rare earth materials, and manufacturing. Such adapting trade flows will prompt companies to engage in the aspect of nearshoring, which is the relocating of operations to a nearby country, and reshoring, that will record operations moving back to the company’s home country, as well as friendshoring, which will see business operations locating to countries with stronger diplomatic and economic ties.

In this context, emerging economies that are in the process of rapid growth and industrialization stand to benefit the most. Brazil, India, and South Africa are strategically positioned near key markets. For example, Brazil can benefit from nearshoring in Latin America for US and European markets, India can serve as a nearshore hub for the Middle East and Southeast Asia, and South Africa is in a good location to serve both African and European markets. This proximity reduces shipping costs and delivery times for companies looking to shorten supply chains. Many of these countries offer competitive labor costs compared to developed markets, making them attractive options for businesses that are moving production closer to their markets without incurring the high costs of fully developed economies.

Brazil, India, and South Africa are seen as stable democracies in their regions with relatively strong governance structures. These emerging economies have also made significant investments in infrastructure, technology, and workforce development, making them more attractive for reshoring activities. India, for instance, is positioning itself as a manufacturing hub under its “Make in India” initiative. Similarly, Brazil has been improving its manufacturing and technological capabilities, while South Africa offers strong industrial capacity in sectors like mining and automotive manufacturing. Moreover, these emerging economies are often insulated from geopolitical shocks largely because of their strategic autonomy, diversified foreign relationships, regional leadership roles, and neutral stances in global conflicts.

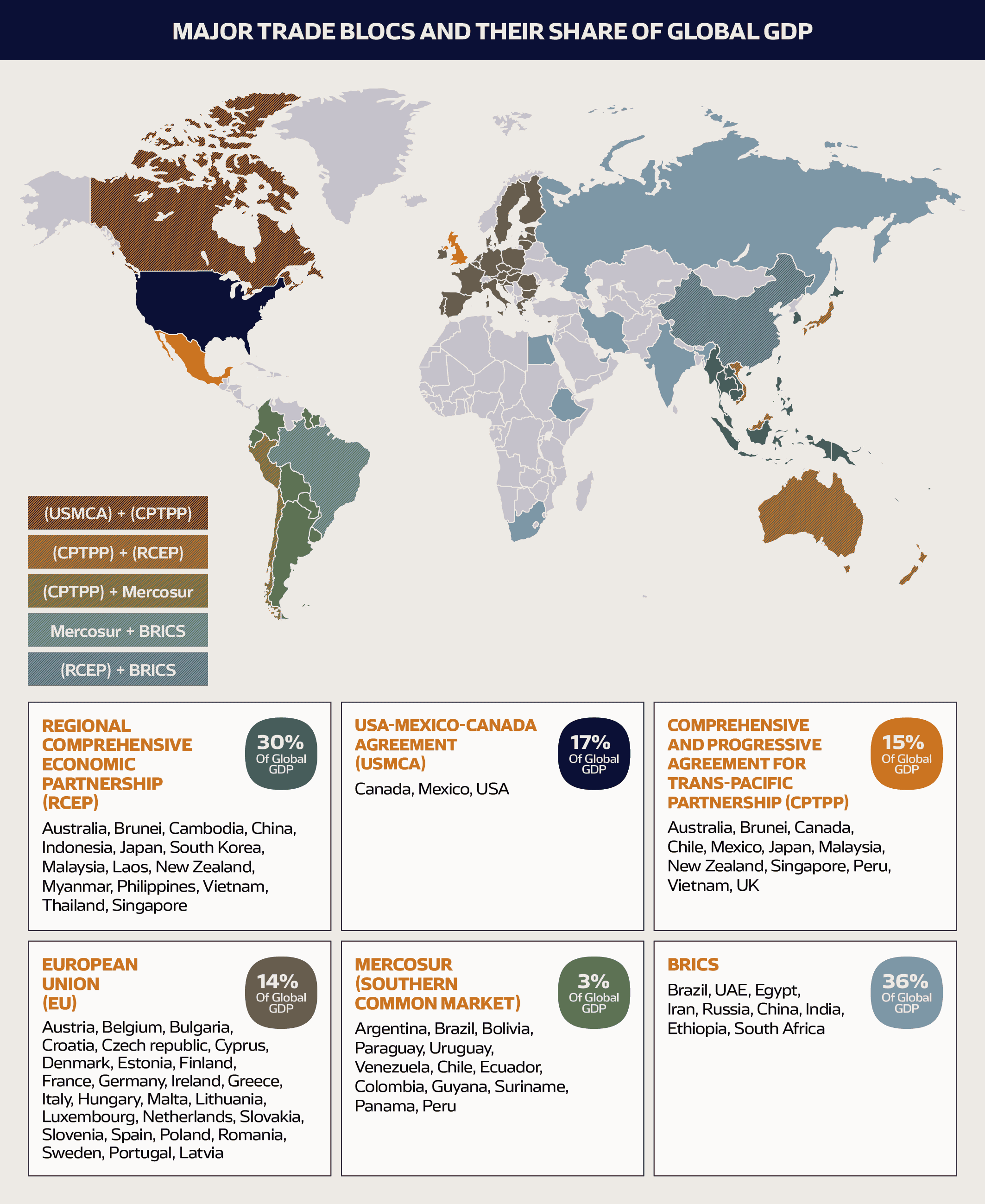

The share of trade occurring within regions is expected to rise as key economic regional blocs like the EU, ASEAN, and North America become more self-reliant. Regional trade agreements such as the European Union (EU), Regional Comprehensive Economic Partnership (RCEP) in the Asia-Pacific, and the African Continental Free Trade Area (AfCFTA) are gaining prominence. These agreements aim to reduce trade barriers, streamline customs procedures, and enhance intra-regional cooperation, thus fostering regional trade. Countries in close proximity will increasingly leverage each other’s strengths, potentially leading to the emergence of specialized industries, such as renewable energy in Europe and technology in East Asia.

As fragmentation deepens, nations will likely shift away from multilateral frameworks, like the World Trade Organization (WTO), toward regional blocs and bilateral agreements to reduce dependency on larger, more protectionist economies. The expansion of BRICS from five to nine members, representing over 36 percent of global GDP, highlights the growing interest in alternative trading blocs. Other regional trade agreements, such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which spans countries across the Pacific, and Mercosur in South America, further exemplify this shift toward regional economic integration.

In conclusion, the global economic landscape in 2025 will be marked by increasing geoeconomic fragmentation, driven by rising protectionism, shifting trade dynamics, and the growing influence of regional blocs. While these developments promise new opportunities for emerging economies, they also pose challenges, including potential slower growth, volatility during the transition process, and uneven resource distribution.