Overview

Former President Donald Trump was re-elected as the US President in the elections in 2024 and is slated to be inaugurated on January 20. MAX forecasts three main scenarios regarding the trajectory of foreign policy to be practiced by Trump and his administration, alongside their likelihood as percentages and impact in 2025. The following sections then explore the impact of the incoming Trump administration in the US on other regions, including Africa, Americas, Asia, Europe, and the Middle East.

Scenario 1: Transactional Diplomacy (65%)

President-elect Trump has distinctively preferred to engage in a transactional form of diplomacy with direct negotiations to secure specific tangible results that would best serve US interests, which reflects his business-oriented mindset. This is transactional diplomacy, which is more pragmatic and result-oriented, which is what Trump is the most likely to engage in to achieve specific goals furthering US interests. Trump has already made eccentric statements, which have included the threat of 25 percent increased tariffs on imports from Canada and Mexico, referring to Canada and Greenland as additional US states. This aligns with Trump’s tendency to engage in bolstered hardline rhetoric, which usually is not reflected in the resultant policy and its impact, with Trump mainly using the rhetoric to gain negotiating power.

Trump’s transactional diplomacy will likely manifest in pursuit of more bilateral trade agreements to achieve maximum concessions including open markets for American goods and services. The incoming US administration will further look to renegotiate and restructure deals with allies in terms of defense and security rather than abandoning these relationships. This is in line with Trump taking a protectionist outlook towards US trade aimed towards growing and safeguarding domestic economy from foreign competition by using measures such as tariffs and sanctions. His administration will look at strategic realignment with both US allies and adversaries to ensure the country’s global interests in terms of economy, security, and politics are served. In his personalized dealings with world leaders, Trump is going to maintain the threat of tariffs and sanctions to extract concessions from countries that are adversaries, like Iran and North Korea, or competitors such as China, as well as allies. Trump’s transactional diplomacy can be expected to have a trickle-down effect, encouraging other countries to also engage in similar diplomatic actions by prioritizing national interests, thus furthering the phenomenon of global geoeconomic fragmentation.

Scenario 2: Unilateral Diplomacy (30%)

A unilateral global foreign policy, which is in line with Trump’s “America First” strategy of putting the US first at the expense of multilateral cooperation and alliances, is more favorable among his domestic supporters. This usually manifests in the form of withdrawals from multinational trade or security agreements, which Trump engaged in during his previous presidency when he withdrew the US from the Paris Climate Accord, the Iran nuclear deal (JCPOA), and the Trans-Pacific Partnership (TPP). This also involves exacerbating trade wars with China, the EU, and other competitors as well as the US grievances over global security contributions. However, this is less feasible in the long term given the interconnected global context with the necessity of maintaining alliances and engaging in global trade to safeguard US security and economic interests.

Trump is likely to continue his “America First” rhetoric but he will not always look to completely disengage with multilateral relations and increase trade tensions, which can damage the US economy. Some of Trump’s foreign policy may have a unilateral approach though it will not be something his administration will rely on every time. Trump will rather use the rhetoric to achieve better negotiating powers while engaging in transactional diplomacy to achieve tangible benefits in interactions with allies or adversaries. This will align with Trump’s focus on economic prosperity for the US, which is going to be difficult in case of retaliatory tariffs and other potential tit-for-tat actions by countries if Trump’s hardline unilateral actions persist, particularly with allies. Given the strategic influence that the US exercises worldwide, full disengagement from the global power dynamics will be detrimental to US interests.

Scenario 3: Full isolationist Diplomacy (5%)

Trump has repeatedly demonstrated his skepticism regarding international organizations and multilateral engagement. There have been concerns that under Trump, the US may witness Isolationist Diplomacy, which would see the US isolating itself from international affairs to focus on domestic growth. However, this strategy is going to be the least probable action taken by the incoming Trump administration in light of the focus Trump has been placing on the growth of American economic interests. His eccentric statements threatening tariff hikes and promises of resolving global conflicts, such as the ongoing Russia-Ukraine conflict, indicate that Trump is going to keep US involved in foreign affairs.

That said, there are still aspects of Isolationist Diplomacy that may manifest as part of Trump’s foreign engagement. This will manifest in the form of potentially reduced military aid, presence, and involvement in various conflicts across the globe. However, the US will not completely stop military support from global security initiatives and rather focus its efforts on major conflicts such as those in the Middle East and the Russia-Ukraine conflict as well as maintain US counter-terrorism efforts. The Trump administration will keep the US interests at the forefront of its foreign policy with Trump’s eccentric rhetoric mainly to be used as a negotiating tool in direct and bilateral engagements with other countries as the US looks to realign with its strategic global partners.

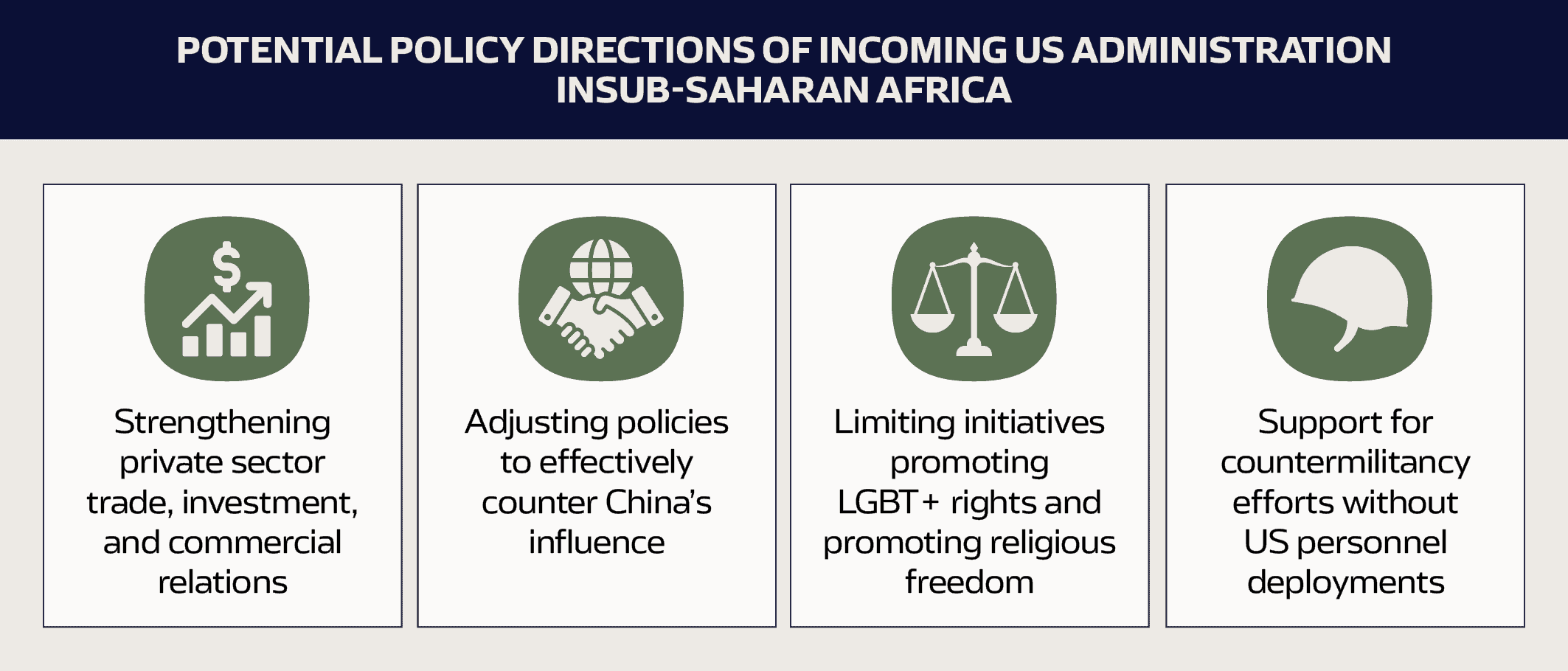

Trump administration to promote commercial economic interests in Sub-Saharan African countries with focus on countering Chinese influence

US foreign policy toward Sub-Saharan Africa is expected to shift under President Donald Trump’s leadership. Central aspects of engagements will be driven by the promotion of commercial interests, economic independence, and strategic competition with China.

The Trump administration will likely focus on strengthening trade initiatives such as the Prosper Africa program, which was established during Trump’s first presidency in 2018 and is aimed at expanding trade, investment, and commercial relations by linking the US private sector to African partners. Since the initiative’s launch, it has helped establish an estimated 120.3 billion USD worth in agreements which the administration will likely look to expand upon to reduce countries’ foreign aid dependence by encouraging self-reliance. A cornerstone of this strategy will likely involve supporting countries’ development of their natural resources, especially oil and gas, to combat poverty and reduce foreign aid, particularly as Trump’s administration is set to halt many green energy initiatives. Beyond this, Trump’s administration has expressed an inclination to cut foreign assistance deemed ineffective, including aid perceived as perpetuating corruption or fueling conflicts. However, the exact execution of this policy remains unclear. The administration is expected to push for an adjusted foreign assistance framework that aligns with pro-market policies and rewards good governance, potentially extending the African Growth and Opportunity Act (AGOA) beyond its 2025 expiration, contingent on countries’ commitment to these principles.

A likely dominant focus of the Trump administration will be countering China’s continued influence in Africa. Beijing’s increasing control over strategic assets, such as ports and mineral resources, is seen as a direct challenge to US global leadership. In response, US foreign assistance programs, including the US Agency for International Development (USAID), will likely prioritize countering China’s “debt diplomacy” by rewarding countries that resist Beijing’s economic influence. The Trump administration will likely also move to increase its dominance in the continent by promoting alliances with fast-growing African economies and leveraging these partnerships to undermine Beijing’s influence.

Trump’s foreign policy is expected to mark a departure from previous administrations’ emphasis on human rights and liberal values in foreign aid and policy priorities. The incoming administration has signaled its intention to limit initiatives promoting LGBT+ rights, viewing such policies as a hindrance to fostering strong relations with socially conservative African nations. That being said, the Trump administration will also likely place a stronger emphasis on the protection of religious freedoms including prioritizing this issue within both diplomatic and aid frameworks, which will align with the administration’s interest in serving its domestic conservative base.

The Trump administration will likely continue support for African military and security operations as seen during Trump’s first term with countries including Nigeria and Somalia. This will likely include training programs and security assistance to enhance the capabilities of African nations to address security challenges, which aligns with broader US goals of preserving stability and combating militancy, particularly in areas affected by extremist groups. That being said, Trump will likely maintain his approach of limiting the deployment of US military personnel.

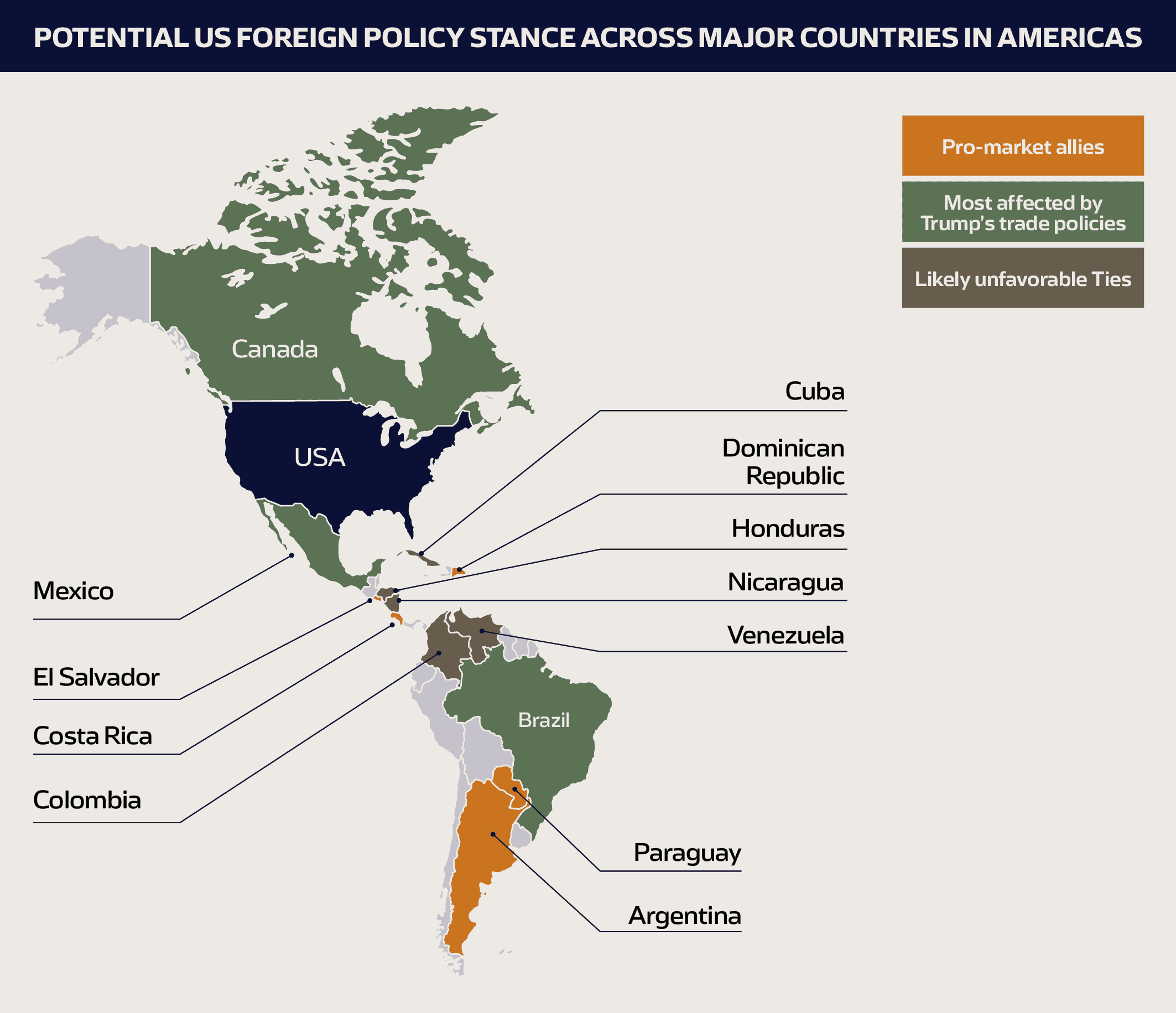

Incoming-Trump administration to prioritize border security, restructuring trade agreements, migration control, while strengthening ties with pro-market allies

The incoming Trump administration is poised to reshape US-Latin America relations, emphasizing border security, trade recalibration, and migration control under the broader “America First” agenda. Trump’s first term revealed a pattern of aggressive rhetoric followed by more measured implementation. This tendency is likely to persist in a second term, suggesting that while Trump may threaten harsh tariffs, sanctions, or trade restrictions on Latin America, the actual impact may be less severe. Consequently, his focus for realigning trade relations will likely target Mexico, Canada, and Brazil.

In this context, Mexico and Brazil are specifically key Latin American economies for realigning trade negotiations, such as reducing trade deficits or increasing US exports in exchange for market access or tariff concessions. Besides being vulnerable to potential trade pressures from the Trump administration, Mexico will face increased US scrutiny regarding migration, drug trafficking, Chinese investment, and the growing trade deficit. Trump will likely leverage the 2026 US-Mexico-Canada Agreement (USMCA) review to gain concessions from Mexico. This heightened uncertainty surrounding US-Mexico relations will likely undermine investor confidence. Given such consequences for renegotiating countries, if Trump maintains his hardline stance regarding import tariffs in trade negotiations, this will potentially prompt some Latin American leaders to pursue countermeasures. These measures could include strengthening ties with China and other global partners or pre-emptively introducing counter-tariffs to insulate the country from a potential US-imposed tariff.

Moving further down south, while the Central American countries are not priority partners for the US in terms of trade, regional security is imperative for Trump to control migratory pressures. Trump’s focus on controlling migration will likely push Mexico to implement stricter border policies, including along its southern border with Guatemala, to prevent migrant caravans from continuing their north-bound journey to the US. Consequently, migrant caravans may be forced to settle for extended periods in Central America. This will further encourage the Central American countries to implement strong law enforcement along their borders. Moreover, mass deportations of migrants from the US to home countries in Central America as suggested by Trump will result in higher unemployment and increased pressures on public services for these countries.

In line with the broader “America First” foreign policy, Trump will likely focus on reducing US involvement in foreign conflicts and limiting financial aid to countries unless there is a clear benefit to US interests. This will likely be exemplified in countries perceived as straying away from hardline anti-drug trafficking efforts. Colombia, will likely be a case in point, with the new National Drug Policy, introduced in November 2023, marking a shift from US-backed strategies by ending forced coca eradication, a move that may strain relations with the US under Trump. Likewise, a similar predicament is likely for Honduras, following the termination of their Extradition Treaty with the USA in March 2024, accusing Washington of “threatening Honduran sovereignty”. Furthermore, Cuba and Haiti are likely to be countries recording similar reduction in US involvement and aid.

Conversely, the Trump administration is likely to strengthen ties with pro-market allies such as Argentina, El Salvador, Paraguay, Costa Rica, and the Dominican Republic. Argentina’s favorable business climate could enhance interest in its energy sector, especially in the Vaca Muerta shale, while its significant mineral deposits, particularly lithium, position it as a crucial US partner in technology supply chains. President Milei may also seek Trump’s support to secure IMF resources.

Moreover, Trump’s focus on deregulation and energy independence could benefit Latin American energy exports, particularly from Brazil, Argentina, and Mexico. His policies may also bolster the Southern Caribbean oil and gas triangle of Guyana, Suriname, and Trinidad and Tobago, shifting away from current US President Joe Biden’s green energy agenda. Venezuela might see eased US sanctions to stabilize oil markets, potentially incentivizing Maduro to accept some refugees. Conversely, Cuba and Nicaragua are likely to face tougher stances, given their limited cooperation with US interests.

Finally, the Trump administration will intensify efforts to counter China’s influence in Latin America, pressuring countries like Peru to limit economic ties with Beijing, particularly in strategic projects like ports, electric grids, and 5G networks. The US may push Latin American nations to serve as alternative suppliers in critical supply chains, reducing reliance on China or to halt Chinese investment in sensitive projects. This shift offers opportunities for industries producing raw materials and intermediate goods for US manufacturing. However, companies should prepare for increased US demand alongside stricter compliance requirements under trade agreements like the USMCA, especially regarding anti-China measures.

Trade conflict with China to sustain, President-elect Trump likely to minimize Washington’s exposure in region’s conflicts

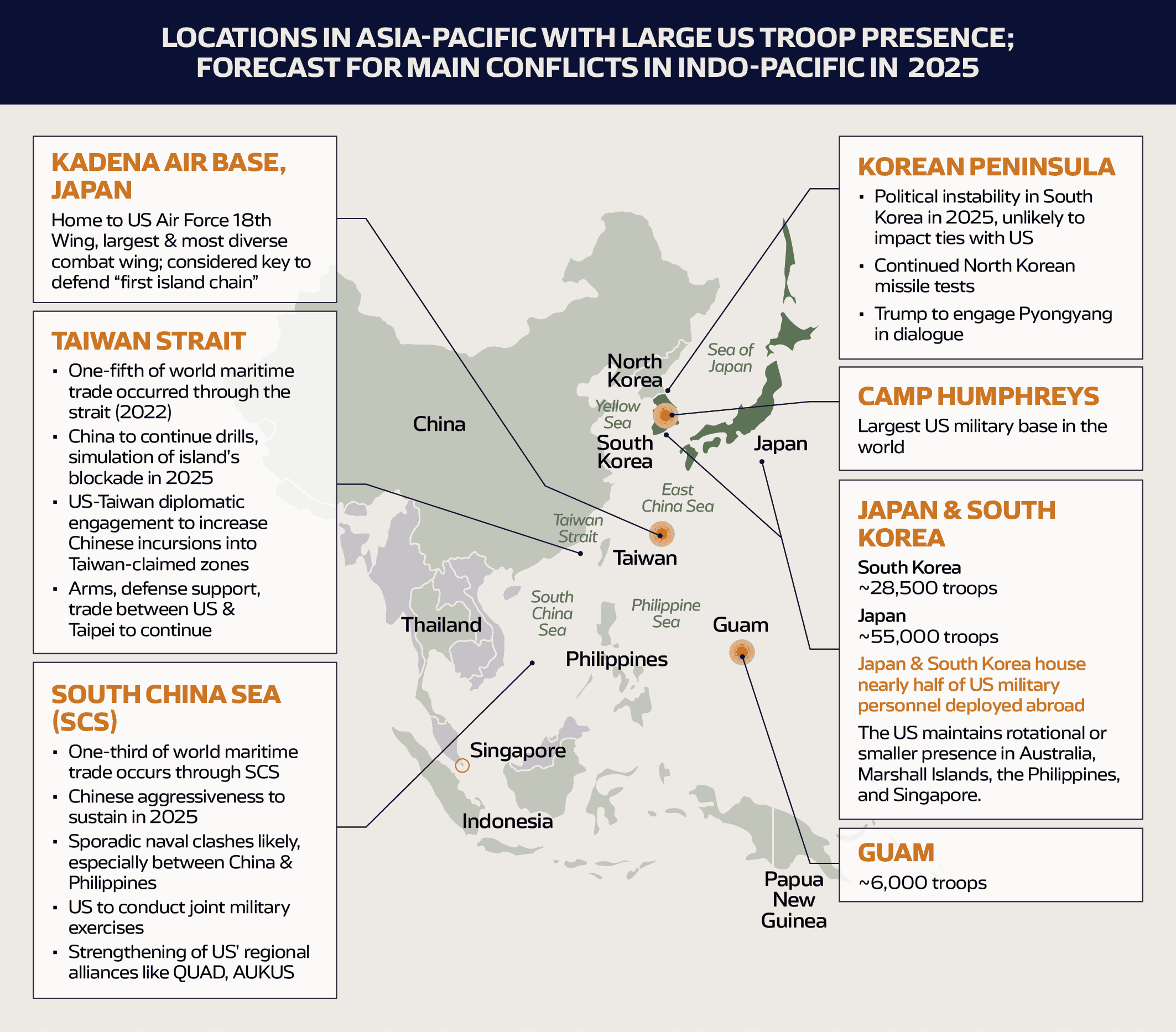

Overall, a broad continuity in foreign policy approaches towards Asia and the Pacific region is expected from the incoming administration of President-elect Donald Trump. The new government will likely continue the previous administration’s focus on “outcompeting” China, consistent with Washington’s rhetoric that the 2020s will be a “decisive decade” for its competition with Beijing. This proactive approach has already been showcased in President-elect Trump’s campaign promise to impose 60 percent tariffs on imports from China. This will extend the ongoing trade conflict between the countries, particularly amid Washington’s existing high tariffs on selected Chinese imports, such as electric vehicles (EVs).

Such tactics will draw retaliation from Beijing, given their impact amid China’s ongoing economic slowdown. Chinese countermeasures will likely include tariffs, sanctions on US entities, and regulatory crackdown on US firms operating in China. Given Trump’s brand of personalized politics, there is also a potential for slight divergences to emerge between his approach and that of his administration. This will largely manifest in rhetoric, wherein the incoming president could publicly project a more hardline stance. That said, both countries will seek to contain the economic fallout from the trade conflict, utilizing diplomatic channels from time to time to de-escalate amid periods of elevated tensions.

Security will also constitute a major consideration of Beijing-Washington relations in East and Southeast Asia. Consistent with Trump’s first term, his administration is likely to facilitate routine diplomatic interactions, streamlined arms sales, and trade agreements with Taiwan. This is expected to prompt an intensification of China’s indirect coercion strategies, known as “grey-zone tactics,” such as aerial deployments in the Taiwan Air Defense Identification Zone (ADIZ), defense drills in the Taiwan Strait, and targeted trade-related measures. Similarly, the South China Sea (SCS) will remain a possible flashpoint amid China’s growing presence in the disputed waters. This will likely elicit a strengthening of the US’ regional alliances, such as AUKUS, which is Washington’s trilateral security partnership between Australia and UK, and the Quadrilateral Security Dialogue (QUAD) with Australia, India, and Japan, as well as joint military exercises.

Further, North Korea is likely to step up its posturing through missile tests while projecting an adversarial approach towards Washington in the near term to hold greater leverage over potential talks on issues such as sanctions. President-elect Trump will seek to build on progress during his last tenure, potentially reaching out to Pyongyang and leader Kim Jong Un to establish dialogue. This will, however, be accompanied by projections of Washington’s military power in East Asia and ostensibly hardline rhetoric to rein in Pyongyang. This is especially likely, should the North amplify its belligerent tactics amid sustained domestic political tensions in South Korea to push its reunification agenda. Pyongyang’s potential aggressive posturing through missile tests, cross-border trash balloons launch, and sporadic cyber-attacks will likely result in Washington deploying aircraft carriers in the peninsula and holding military drills with the South and Japan.

That said, the US is likely to prioritize other more pressing conflicts, such as between Russia-Ukraine and in the Middle East in its foreign policy agenda. Thus, significant US-led escalations are less likely in Asia’s theatres of regional power contestation. While this does not signify a full-scale rollback, President-elect Trump is more likely to favor a general limiting of major US intervention in conflict hotspots in Asia to offset Washington’s potential overextension.

Meanwhile, in South Asia, Trump’s perception of India as a crucial partner to counter China will prompt the new administration to respond relatively favorably to New Delhi. On the other hand, Pakistan is likely to face military aid cuts amid a general souring of relations between Islamabad and Washington due to possibly asynchronous approaches to countering militancy. The new administration is unlikely to lodge itself in political conflicts in Central Asia or the South Caucasus, opting for a less hands-on approach considering its preoccupation with other global security concerns.

European countries to increase defense spending, push for economic protectionist policies to reduce dependence on USA in 2025

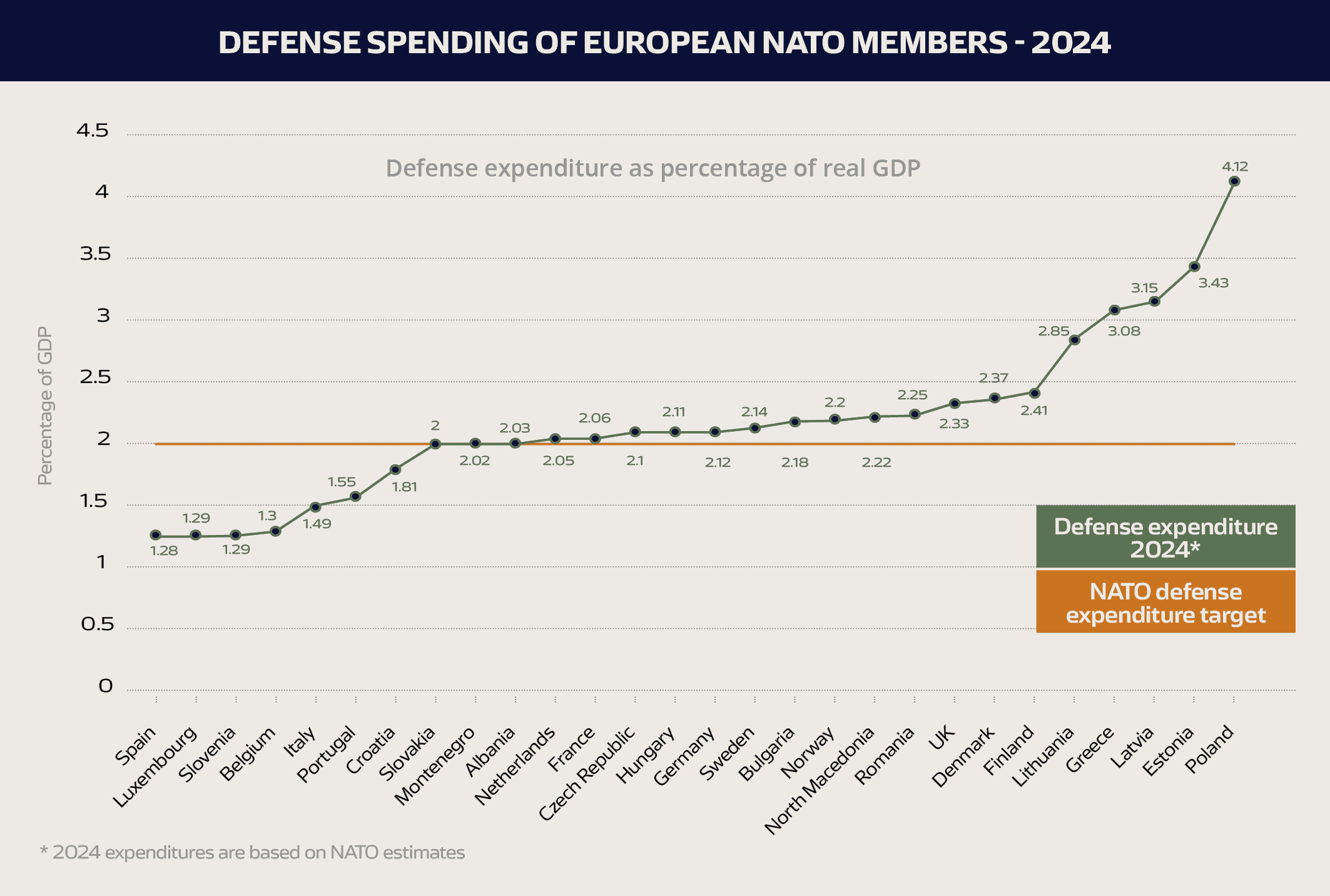

US President-elect Trump’s second term will significantly impact Europe in 2025 given the unpredictability of his foreign policy. His “America First” campaign will take a protectionist and isolationist foreign policy stance, including toward NATO. Trump has repeatedly stated that he would leave NATO if financial commitments from other partners were “unmet.” He has also maintained he would not defend countries that failed to meet these commitments if Russia attacked, despite NATO’s Article 5 of collective defense. While NATO’s minimum defense spending target for member states is two percent of GDP, Trump reportedly wants the target to be raised to five percent, increasing pressure on European states.

With US security support not guaranteed under Trump, European countries will likely offset the potential negative impact on its security by ramping up efforts to raise their defense capabilities in 2025. This is especially likely considering the heightened threat of Russian hybrid warfare and destabilization activities in Europe, coupled with Moscow’s amplified threats of nuclear escalation in late 2024.

Countries bordering Russia have already steadily increased their defense capabilities and war preparedness since Russia’s invasion of Ukraine in February 2022. Poland allocated three billion EUR to defense in 2024 and is set to allocate 43.6 billion EUR of its 2025 budget to defense, representing 4.7 percent of its GDP. Similarly, the Baltic countries – Estonia, Latvia, and Lithuania have all set a target of raising defense spending to at least three percent of GDP, with Latvia and Estonia estimated to have met the threshold in 2024. On average, defense budgets in Europe increased by nine percent in 2024, estimated at some 414 billion EUR in total.

Governments in the Nordic countries are also boosting defense spending in their 2025 budgets, with other European countries liable to follow suit in their respective budgets. However, the increase in defense spending will require cuts to welfare and public services, which will likely complicate efforts to pass budgets and legislation to grow defense capabilities. Considering the already increased political fragmentation and polarization in multiple European countries, this is likely to trigger political instability due to intra-coalition divisions and, potentially, no-confidence motions against the ruling governments. Such developments were already seen in 2024, with the collapse of the German and French governments due to budgetary divisions, including regarding military aid for Ukraine.

Moreover, in the event of scaled-back US support, Europe would lack the armed forces and equipment needed for High-Intensity Warfare (HIW). Consequently, Europe is likely to focus on building a joint defense-industrial base, with the EU likely to play a central role. President of the European Commission (EC) Ursula von der Leyen has made building a “European Defense Union” a priority, with reports suggesting the EC will allocate up to 130 billion EUR from its seven-year common budget to military-related programs. In addition to this, European countries are likely to continue pushing for a voluntary joint defense fund involving non-EU members such as Norway and the UK.

Europe is also expected to focus on collective economic policies to make the region more competitive and less dependent on the USA. In September 2024, former President of the European Central Bank, Mario Draghi, presented a report titled “The Future of European Competitiveness”, detailing a plan to boost growth and competitiveness. The plan calls for removing single market barriers for EU businesses and raising annual investment by 800 billion EUR. While the plan was initially met with skepticism from Brussels over the scale of investment, it is likely to see increased support from EU members in 2025, amid growing concerns over a possible USA-China trade war. Indeed, 20 EU members already signed an initiative to remove barriers to the EU’s single market in response to the report.

In response to possible US tariffs, the EU is likely to take on more protectionist measures for certain industries, with EC vice-president Stephane Sejourne calling for a “Europe First” strategy to protect the EU from becoming a “collateral victim of a global trade war.” These industries include steel, automobile manufacturing, aerospace, and clean technologies. However, considering divisions within the EU, particularly with populist leaders supportive of Trump, such as Hungary’s Victor Orban and Slovakia’s Robert Fico, the bloc will face considerable challenges in passing legislation needed to insulate Europe from a potential trade war, and thereby ensure economic security in the region.

President-elect Trump’s Middle East Policy expected to be transactional vis-a-vis allies, hostile toward Iran

A primary aspect of President-elect Donald Trump’s Middle East policy will be Iran. Washington’s policy toward Tehran and its proxies will likely build on his previous “maximum pressure” approach. Iran’s reported attempts to assassinate Trump on US soil, as well as efforts to disrupt his electoral campaign, are likely to reinforce Washington’s hardened foreign policy posture toward Tehran. Under the “maximum pressure” framework, Trump is likely to reinstate and intensify economic sanctions targeting critical sectors of Iran’s economy, such as oil exports and financial systems, primarily to curb Tehran’s revenue streams and compound Iran’s economic crisis. The administration will also leverage more strictly secondary sanctions to derail global companies and countries from facilitating, even tacitly, Iran’s sanction circumvention tactics, which Tehran has utilized in recent years.

A primary foreign policy interest for the new administration will also be Iran’s current escalation in terms of uranium enrichment, which already led President-elect Trump’s transition team to consider military options to derail Iran’s nuclear project. While this partially contradicts Trump’s stated inclination to avoid getting embroiled in wars, his administration will likely align with Israel’s view of Iran’s nuclear project as a paramount national security threat. Members of Trump’s transition team have also referenced the geopolitical ramifications emanating from Israel’s extensive degradation of Hamas and Hezbollah and the fall of al-Assad’s government in Syria, which have significantly weakened Iran. This will bolster the new administration’s alignment with the Israeli view and conviction that there is now a strategic window of opportunity to strike Iran’s nuclear project. This is a vision that will likely be strongly shared by the US’s other Middle Eastern allies, referred to as the “moderate axis” of countries that perceive Iran as a direct threat. This particularly includes Saudi Arabia, the UAE, Bahrain, Jordan, the anti-Houthi camp in Yemen, and the anti-Hezbollah camp in Lebanon, all of which will likely lobby for a firm US posture against Iran, even if tacitly. To this end, the Trump administration will likely deploy assets to reassure the anti-Iran regional camp, bolster the latter’s collaboration and mutual defense mechanisms, and compound Israeli military plans to target Iran.

This will undergird and increase friction between US forces and Iran-backed regional allies, with Iraq and Yemen constituting the primary flashpoints for hostilities, which are liable to adversely impact the Gulf through eruptions of cross-border missile and UAV attacks by Iranian allies. In this context, the US Central Command (CENTCOM) will resort to direct military action to hinder Iran’s proxies and allied groups, and Washington will likely expand the use of economic sanctions to target these proxies and their financial networks, primarily to disrupt the funding sources that sustain them.

With the US’s regional allies, primarily the Gulf states, the new administration will continue to reflect his previous approach, characterized by strategic alignment and transactional relationships, with pragmatism regarding these states’ human rights records. Unlike during Trump’s first term, when the Qatar blockade heightened tensions among Gulf states, the current improved cohesion among Gulf states will likely enable a more unified engagement with Washington on key Gulf Cooperation Council (GCC)-related issues. Trump will likely prioritize securing tangible benefits for the US, such as large-scale defense contracts, energy cooperation, and investment in American infrastructure and industries. A significant focus will also include engaging directly with these states to influence OPEC+ decisions, mainly to prevent high oil prices that could strain the global economy and US consumers. His administration would likely continue promoting large-scale arms sales, framing them as essential for regional security against Iran, terrorism, and other threats. However, such support will likely be conditional on their alignment with US interests, such as countering growing Chinese influence. Concurrently, Trump will also focus on bringing additional GCC states, particularly Saudi Arabia, into signing normalization agreements with Israel. This will likely be done by offering robust security guarantees and support for Saudi’s defense and economic programs.

Trump’s policy toward Israel is expected to remain strongly supportive, further solidifying the strategic partnership across security, diplomacy, and economic collaboration. The administration will hold a significantly more hostile approach toward Palestinian factions. With regard to the war in Gaza, this will be characterized by a hands-off approach to allow Israel to extend as much military pressure as it deems necessary on Hamas, to bring the latter to accept its truce terms.