Executive Summary

-

On September 13, US President Joe Biden’s administration imposed tariffs on several Chinese goods, mainly in the domain of green technology products which are used to generate clean energy as well as critical minerals needed to make these goods.

-

These tariffs have been imposed to counter Beijing’s years-long dominance in the critical mineral supply chain, which has made US firms increasingly reliant on China to acquire these resources. The tariffs are made to reduce such reliance and make the US more competitive in its larger geopolitical competition with China.

-

However, these measures will likely take years to come into effect even as China maintains its dominance over the mineral supply chain. Meanwhile, both the US and China will likely take reciprocal measures against each other, increasing the cost of critical mineral supplies and green technology, potentially slowing down the green transition in the coming years. .

-

Businesses are advised to remain cognizant of developments regarding the US-China green technology trade war and allot for disruptions to the supply of green technology and critical minerals as Washington and Beijing look to compete for influence over green technology across the globe.

Background

On September 13, the US announced tariffs ranging from 7.5 to 100 percent on Chinese products including electric vehicles (EVs), solar panels, and semiconductors to be effective from September 27. This comes after US President Joe Biden announced a series of revisions to existing tariffs on multiple products imported from China in May.

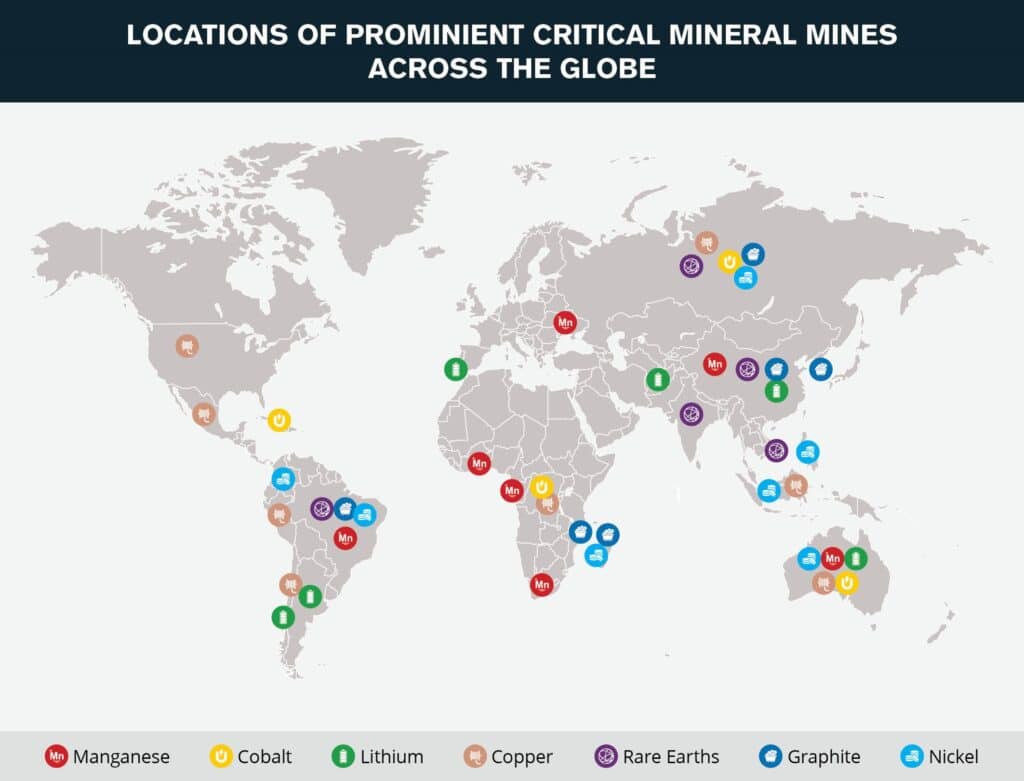

Most of these tariffs were applied to “green technology” and “critical technology” products or minerals used in the manufacturing of these products. Green technology comprises products that are used to either generate clean energy or replace polluting technologies and products with those that have net zero emissions. Such products include solar panels, wind turbines, electric vehicles, and lithium-ion batteries. Most of these products require critical minerals such as lithium, cobalt, manganese, and nickel which are found in reserves across the globe. These minerals need to be excavated, processed, and refined for use as components in the final green technology products.

Biden stated that these tariffs were being revised to counter China’s dominance over the global mineral as well as green technology supply chains, and he called upon his trade representative to enhance the US’s supply chain resilience. These tariffs escalated a brewing commercial conflict between the US and China over green technology and became part of the larger US-China geopolitical rivalry for influence over the global economy and political landscape.

Overview & Outlook

Chinese dominance over critical mineral supply chains, green technology products to impact Western economies, geopolitical leverage

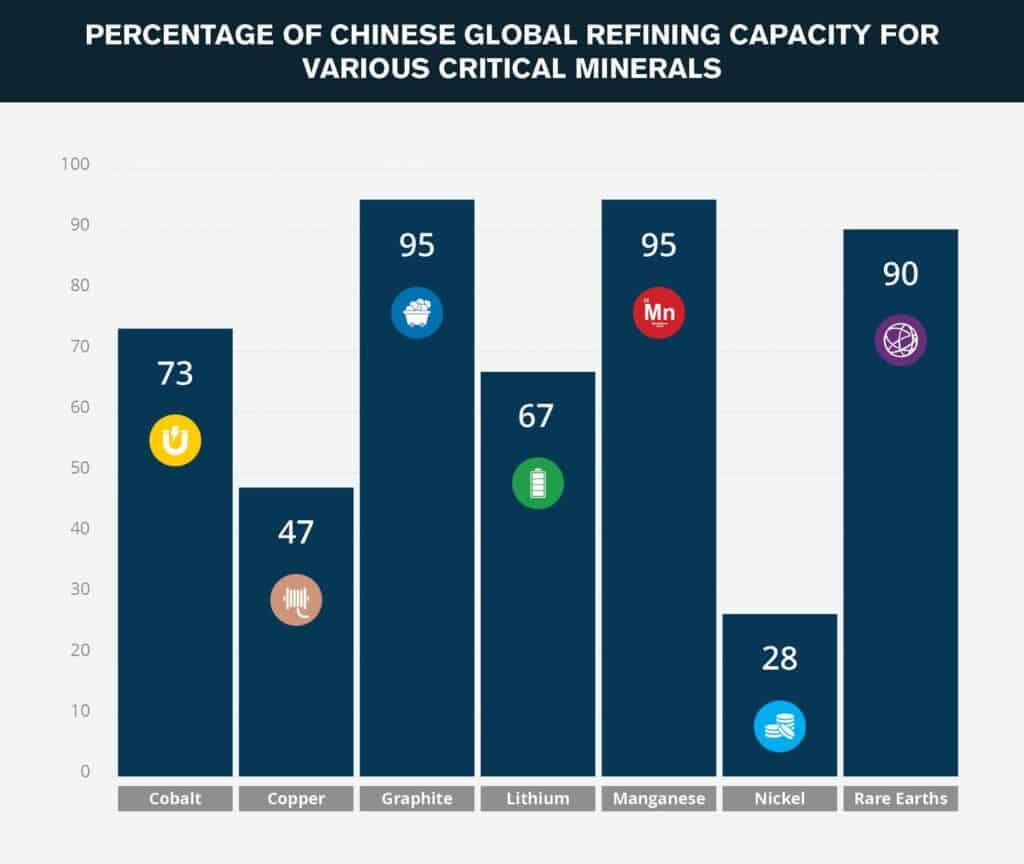

Over the past decade, China has steadily acquired dominance over crucial mineral supply chains and green technology products. This is evidenced by the fact that Chinese firms are responsible for 60 percent of the worldwide extraction of such minerals and 85 percent of their processing capacity. The high extraction rates can partially be explained by China’s significant domestic reserves of such minerals and skilled labor as well as technological capabilities to efficiently mine the minerals. This is in contrast to the US, which generally has smaller reserves of minerals such as graphite. However, China does not have reserves of all minerals, especially nickel and lithium. To make up for this, in the past few decades, Chinese firms have assiduously developed relationships with Chile, DRC, Indonesia, and other nations that have significant reserves of these minerals. China has incentivized these nations to allow Chinese firms to exclusively extract and even refine these minerals, in exchange for implementing development projects and assisting the countries in developing downstream manufacturing capabilities. While the US has also tried to follow such an approach, particularly with lithium mining in Afghanistan, these efforts have been sporadic or failed due to geopolitical developments such as the Taliban takeover of Afghanistan.

These exclusive mining rights have allowed Chinese firms to extract a critical mass of minerals for the production of green technology. This dominance over global supply chains of required minerals comes in tandem with Beijing’s attempt to increase the contribution of green tech manufacturing to China’s GDP, with the Chinese government investing 890 billion USD in clean energy investment in 2023. The Chinese government sees this investment as crucial to spurring growth, especially since previous growth-propelling sectors such as real estate have been undergoing a downturn since 2022. This investment has come in the form of subsidies for companies developing green technology and providing land to build factories that can manufacture green products, among others. These incentives, along with Chinese firms’ abilities to source building materials through Beijing’s dominance of supply chains, have lowered the costs of production. Consequently, the low cost of production has contributed to China’s dominance over the production of green technology such as solar panels, windmills, and electric vehicles (EVs) as well as crucial technology such as batteries. This is seen in China’s share in all stages of solar panel manufacturing being almost 80 percent, including a 97 percent share in the production capacity of global silicon wafers, the material needed to process solar photons to energy.

Despite this excess capacity and production capabilities, domestic consumption and demand in China is relatively low at around 53 percent of GDP when compared to an average of 75 percent of GDP in other nations. This anomaly has pressured Chinese firms to export excess products to global markets in Europe, the Americas, the Middle East, and Southeast Asia. Given the low costs of production, and the need to sell green products in the absence of a robust domestic market, these Chinese firms sell their products at a low cost. This raised questions about these firms dumping, or selling products at such a low cost to sell excess goods creating concerns among Western governments about their consumers becoming dependent on Chinese products and technology.

This dependence has the potential to put Western firms at a competitive disadvantage and make Western governments weaker in their response to the larger geopolitical competition with China, which includes rivalry over political as well as economic influence across the globe. However, if Western countries adopt legislation or policy to prevent such a scenario, aimed at reducing Chinese influence over mineral supply chains, Beijing will likely threaten to adopt retaliatory measures such as export quotas or restrictions on sales of green tech products. This would create a severe shortage of not just green technology but even other crucial products such as batteries and minerals such as lithium involved in manufacturing across various sectors across Western nations. These minerals are often used in the production of various vital technological goods such as phones and laptops, and are crucial in the transition to sustainable energy. Thus, shortages of these goods have the potential to disrupt economic activity in Western nations and lead to an adverse impact on growth and employment.

Imposition of tariffs to have limited impact on energy transition, Chinese green technology capabilities

The US is aware of the dangers of dependence on China for its green technology, which explains Biden’s imposition of tariffs. These are intended to prevent a dependence on the import of critical minerals and technology from China while incentivizing US companies to upscale and directly compete with Chinese products on the global market. This can be seen with the various caveats in the imposition of these taxes. For example, the tariffs on electric vehicles are the highest and are to be implemented in 2024. This is because the US already has various auto companies with the technological know-how to build electric vehicles. Thus, the US can afford to impose such tariffs, which would make even relatively cheap Chinese EVs prohibitively expensive, without impacting its residents. On the other hand, the tariffs on graphite and lithium battery storage are at 25 percent and only come into effect in 2026. This is because the US continues to rely on China for the import of these minerals, with American capacity to mine graphite in particular being null. The US is still in the process of diversifying its supply chains over these minerals, and thus the two years until the tariffs come into effect give Washington time to solidify its supply chains. Moreover, China is aware of this dependence and can use perceived hostile actions from the US to restrict exports, as seen in an export ban on rare earth minerals in December 2023. Thus, the relatively low tariffs also allow the US to not antagonize China while allowing companies to import graphite from China in case of shortages without extremely large costs.

However, there are complications to the tariffs being fully effective in challenging Chinese dominance in the mineral supply chains and limiting its exports of green technology exports. For one, in the past few years, China has rerouted supply chains for various green technology products such as solar cells and electric vehicles (EV) through countries that are friendly to the US including Mexico, Malaysia, Thailand, Morocco, and South Korea. However, these countries maintain strong economic ties with China as well and are unlikely to buckle under potential US pressure to cut down on ties with Beijing. To this point, Chinese firms have set up production factories in these nations to export their products to the US. This allows the Chinese firms to bypass the tariffs because of regulations within the subsidies given to manufacturers to improve the production and sale of various green technologies through President Biden’s Inflation Reduction Act (IRA), 2022. The IRA mandates that a certain percentage of the extraction and processing of critical minerals as well as the components of batteries used in EVs must be in the US or in a country that has a free trade agreement with Washington to take advantage of the subsidies. Thus, rerouting through US-friendly countries allows China to take advantage of subsidies to undercut the recent tariffs and continue supplying to the US.

This situation creates a dilemma for the US since it could pressure friendly countries to not allow China to set up factories on their land. However, this risks a backlash from these countries given the potential economic benefits of Chinese investment. While the US could threaten to revoke these nations’ IRA benefits, it could negatively impact relations with diplomatically friendly nations and leave the US with fewer allies when determining its geopolitical strategies and actions. The US is aware of this and might look to tighten restrictions and issue clarifications to further restrict Chinese firms from taking advantage of these subsidies. This can somewhat be seen in the US Treasury’s release of a statement on the definition of the “Foreign Entity of Concern” designation (FEOC) on May 3. The FEOC is a stipulation within the IRA that broadly disqualifies entities deemed to potentially pose economic or security threats to the US from being eligible for financial incentives and tax credits. In this context, the US Treasury announced that if 25 percent of equity, voting rights, or board seats in a company in an automaker’s battery supply chain is held by a Chinese government-linked firm, the automaker’s IRA tax credit will be revoked.

However, while this limits the routes through which Chinese companies can sell their products into the US market by setting up factories in US-friendly nations, three broad problems for the US emerge from these restrictions. For one, at this time US companies continue to rely on China to secure the supply of critical minerals in green technology productions. So while the tariffs and state subsidies to US firms are intended to reduce Chinese competition to US green technology manufacturers, and give them space to increase sales of various products in the American market, they also increase the costs of import of critical minerals for US companies. This will likely increase production costs and make the US companies allocate subsidy resources to simply buying material instead of expanding capacity, at least until the US secures its supply chains and reduces dependence on China for critical minerals in the coming years.

Moreover, a lack of Chinese product competition in the US market could make US firms complacent in enhancing capacity because these companies would have little motivation to innovate over the belief that there would always be demand for their product. This would not only delay the green transition in the US but also make US green technology firms uncompetitive on the global stage. On the other hand, Chinese firms will likely look to sell goods to emerging economies where demand is rising for green products and batteries, such as Vietnam, Indonesia, Brazil, and other Global South nations to offset losses from the US market. This will allow Chinese companies to continue producing green technology while also increasing China’s influence across nations in Asia, the Middle East, and Latin America, putting Washington at a disadvantage in its overall strategic competition with Beijing.

FORECAST: The US is likely aware of this potential outcome on its green transition and influence across the world and will continue to work on diversifying its supply chains and reducing dependence on China when it comes to access to critical minerals. It has already somewhat started this process through several measures including making mineral-rich Canada and Australia eligible for a Defence Production Act, which would see US financial support for mining projects in these nations in May 2023. Such a project could make it easier for the US to obtain these minerals without having to purchase them from China while also providing some competition to US firms to prevent complacency. These efforts will continue, with the US likely to also attempt to build relationships at the state and company level to further get minerals in Chile, Australia, DRC, and other nations to offset mineral reliance on China.

FORECAST: However, these measures will likely take years to take shape, and until then US firms will likely continue purchasing minerals from China. To this end, the US will likely balance its imposition of tariffs while also not increasing restrictions on the import of critical minerals. This is likely intended to prevent supply chain disruptions due to these restrictions from severely impacting the production of green technology and batteries which are crucial for the working of all green and electronic devices. On the other hand, China will also seek to maintain its dominance in the extraction and processing of minerals. Beijing might impose retaliatory measures which could include export restrictions, quotas, or taxes on trading with US firms in the coming months, thereby increasing its influence and strategic competition with the US.

Recommendations

-

Businesses are advised to remain cognizant of developments regarding the US-China green technology trade war and allot for disruptions to the supply of green technology and critical minerals as Washington and Beijing look to compete for influence over green technology across the globe.

-

For any questions and risk assessments, please contact intel@max-security.com.